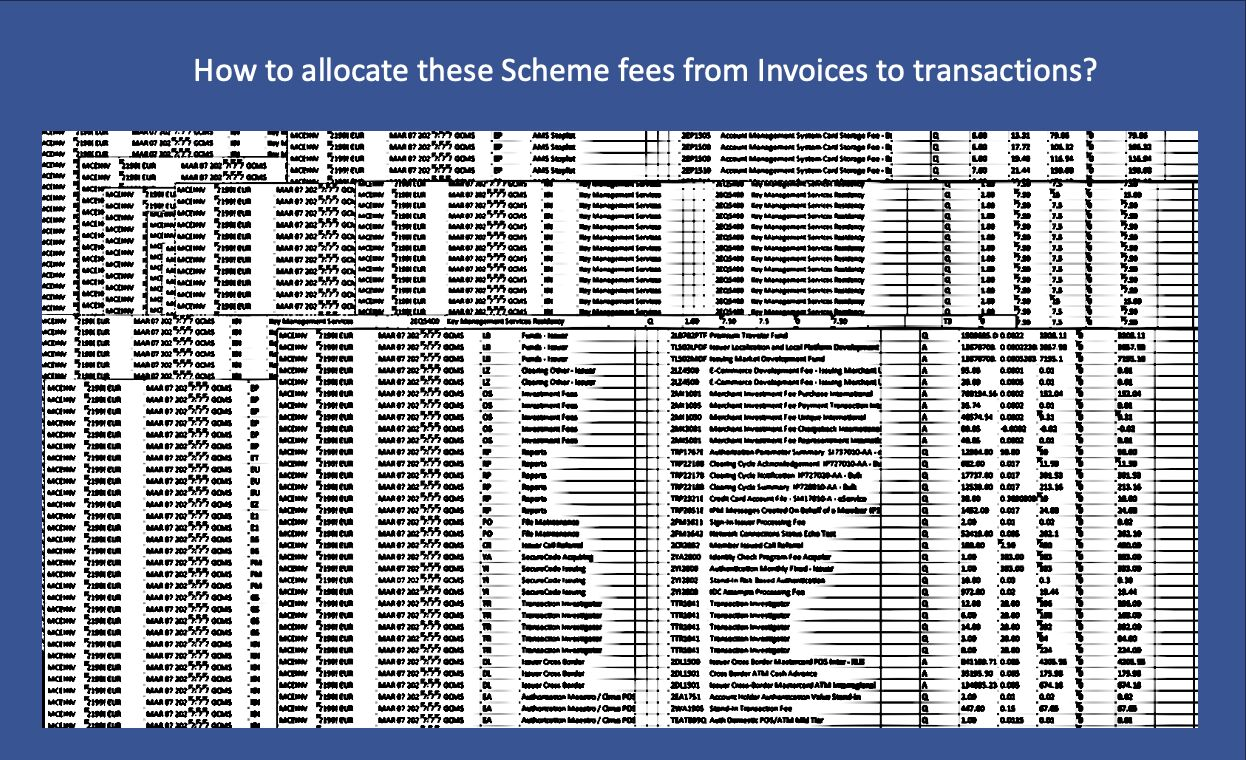

One of the most common misconceptions in card acquiring is that payment scheme fees can be accurately allocated to transactions simply after receiving an invoice from Visa or Mastercard.

In reality, the situation is far more complicated.

Recently, we discussed this topic with a representative of a major European merchant operating across multiple markets. The conversation focused on one critical issue: the lack of transparency in scheme fee calculation and allocation.

A common assumption is that because schemes invoice acquirers weekly, monthly, or quarterly, fee allocation can only happen retrospectively after settlement documents arrive.

But invoices themselves rarely provide the level of granularity required for transaction-level analytics.

Scheme fees are usually delivered in aggregated formats — grouped by fee category, pricing logic, or reporting bucket.

Unlike interchange, where transaction-level settlement reporting may be available through dedicated acknowledgement files, scheme fee reporting does not typically include the same analytical depth.

As a result, market participants are forced to build their own internal allocation methodologies.

Acquirers, PSPs, merchants, and analytics providers often use different logic models, assumptions, and reconciliation approaches. This means there is no universal industry standard for calculating scheme fees at transaction level.

And this is exactly where many profitability and margin visibility challenges begin.

Understanding payment economics today requires more than settlement data — it requires a unified analytical approach capable of connecting fragmented fee structures across the entire payment chain.